Opening corporate accounts at banks is a laborious process which contains multiple friction points. With such a tough KYC challenge on their hands, it is not just the customers that can be disillusioned by a poor customer experience, but the bank themselves suffer from poor processes.

With data stored sporadically, not shared amongst different banking departments, this incomplete data leads to an unfulfilled KYC roadmap. Coupled with the fact that customers themselves may not provide sufficient data, and that manual tasks are littered with human error, these factors can all cause lengthier operations to fill in data gaps. Oliver Wyman notes that the average onboarding time for corporate banking customers can be up to a staggering 120 days.

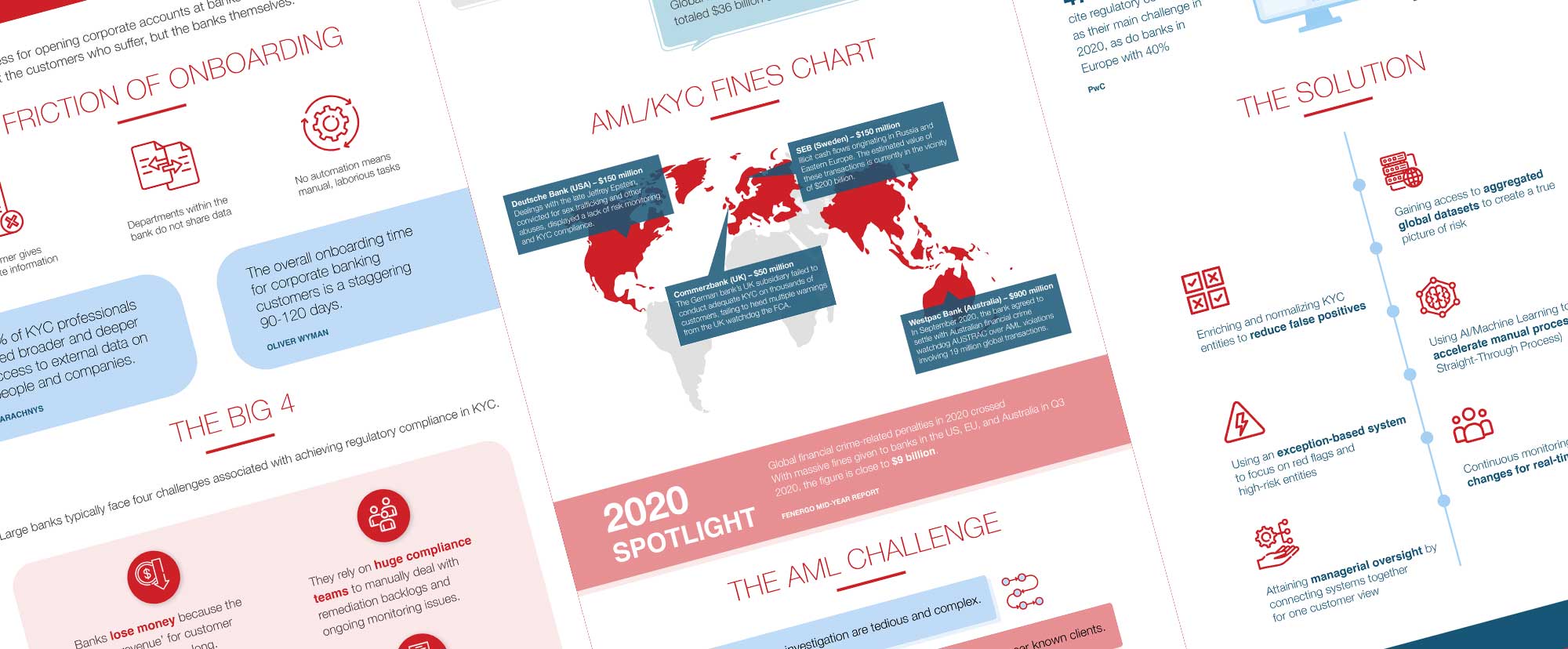

These roadblocks can cause even greater issues for banks: the loss of money when time to revenue is increased, and subsequent AML fines for non-compliance with strict money laundering regulations. Last year saw worldwide fines handed to financial institutions from the United States of America to Sweden to Australia, all due to improper risk monitoring and a lack of KYC compliance.

There are solutions available however, notably the enriching and normalizing of KYC entities and the use of AI and machine learning to automate previously manual KYC processes, all through the Arachnys platform.

This handy infographic details the problems banks and their customers face throughout onboarding, and how these can be rectified.